The Good

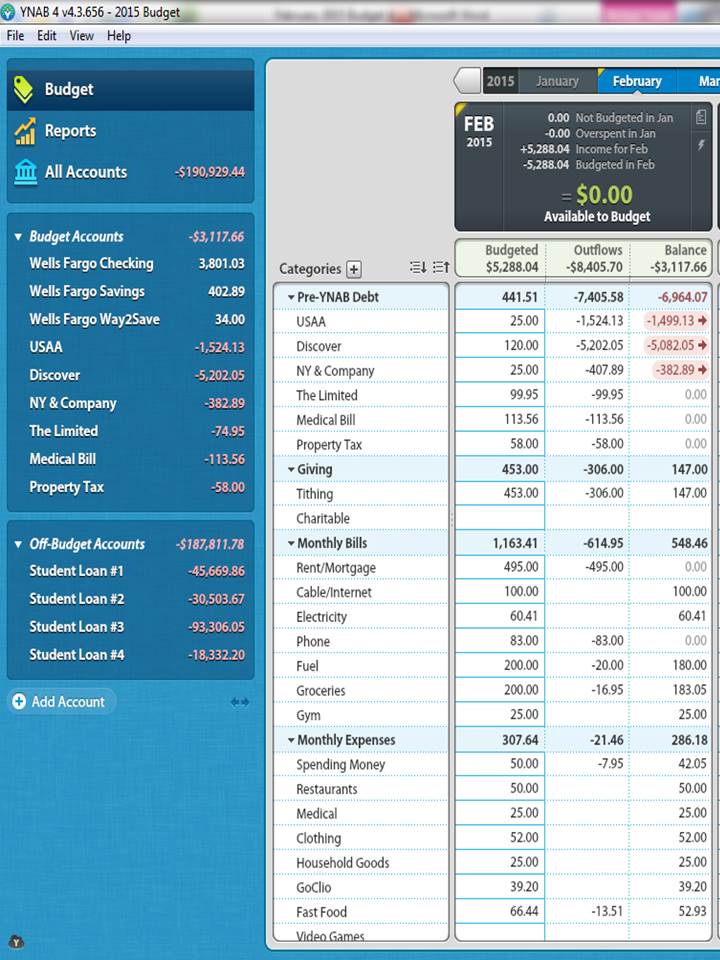

Technically, I have yet to go over budget in any category this month so yay me. I have stayed away from the mall and some of my favorite stores to ensure that I am not tempted to buy new things. I also have to delete the sales e-mails I receive…I swear they know I am trying to cut down on my spending and want to tempt me with all kinds of sales (ugh).

Also, I have the opportunity for a new position that pays almost double my current salary, includes benefits and locality pay and is in an area of law that I think I would actually enjoy. I would have to move, which is time consuming and expensive, but I think it would totally be worth it for the increased salary. As I would be moving to a more metropolitan city, I would have to run the numbers to see just how much it would cost to live in the new city (or maybe not far outside the city) and whether I could live on what I make now and use the remaining funds to pay off my debt and build up my savings.

The Bad

I found expenses that I failed to budget for this month. Luckily, none of these expenses were large amounts (which is probably why I forgot about them) and there weren’t many. In order not to go over budget, I pulled funds from other categories that I knew I probably wouldn’t use this month. I’ll have to rework my budget for next month. (Some good news though, is that some of the expenses I can put an end to so I won’t have to pay them anymore.)

The Ugly

I have basically blown through my fast food and restaurant budget within the first week of this month. I have a few dollars left in both, but not much lol. Part of the reason is because I didn’t really cook last week so that meant a lot…whole lot…of eating out. Again, I haven’t gone over budget (so far), but it is something that I will need to take in consideration for next month’s budget.

Final Thoughts

Overall, it has been a good first week. I haven’t gone over budget in any category and I have an opportunity for a new job with a substantial pay increase, which means more money to put towards my debt. As I am more conscious of my eating out habit (thank you YNAB), I am making an effort to cook more this week so I can save some money. I am glad the month is starting out well…it gives me hope for the rest of the month :).

How is everyone month’s coming along so far? Are we sticking to our budget?